Key Takeaways

- Strategic Shift: Generali is positioning itself to replace AXA as the wealth management partner for Monte dei Paschi di Siena (MPS), aiming to bring Italian household savings back under domestic control.

- Market Scale: Italy’s private banking market is on a structural growth path, with total assets under management (AuM) projected to exceed €1.4 trillion by 2026.

- Demographic Catalyst: The "Great Wealth Transfer" will see approximately €300 billion in assets pass to younger generations by 2033, creating a massive opening for domestic wealth advisors.

- Economic Sovereignty: This move is more than a corporate deal; it is a push for "financial sovereignty," ensuring that the core capital of Italian families remains a strategic asset for the nation's economy.

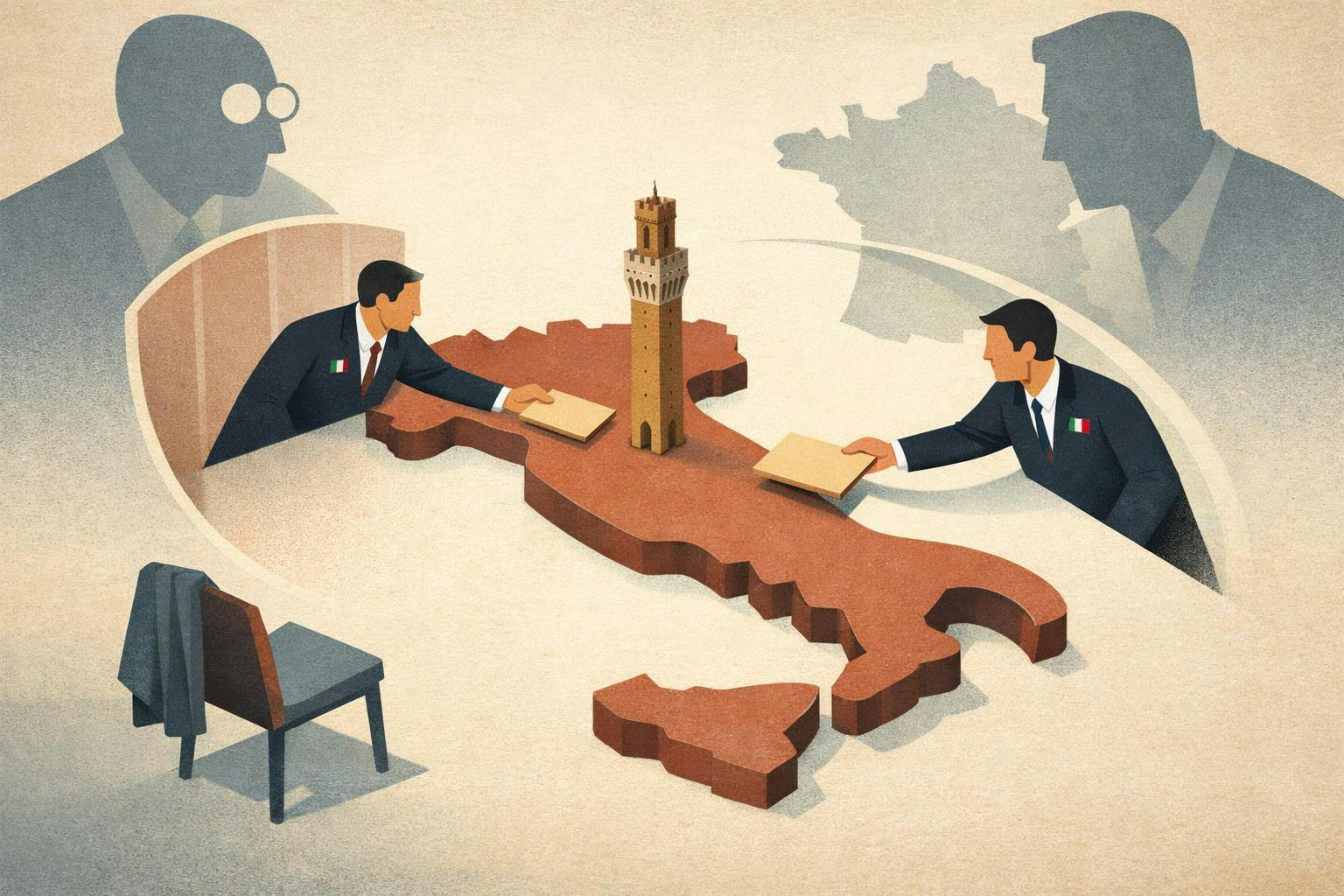

For decades, the management of Italy’s vast private wealth has been a fragmented affair, often overseen by a mix of local banks and giant foreign insurers. However, a significant shift is currently brewing in the boardrooms of Milan and Siena. Assicurazioni Generali, Italy’s largest insurer and a cornerstone of its financial system, is signaling a bold ambition: to reclaim the management of Italian household savings from foreign competitors.

This isn't just a quest for higher fee income; it is a pursuit of financial sovereignty. By seeking to replace the French insurer AXA as the wealth and insurance partner for Banca Monte dei Paschi di Siena (MPS), Generali is attempting to consolidate the domestic wealth landscape. In an era where "strategic autonomy" has become the mantra for European nations, Generali’s move suggests that who manages a nation’s savings is just as important as where that money is invested.

Boardroom Chess: The MPS-AXA-Generali Triangle

The current partnership between MPS and AXA is a long-standing joint venture that covers both life and non-life insurance products. However, this agreement is set to expire in 2027, creating a strategic window that Generali appears eager to exploit. The Generali MPS partnership would represent a monumental consolidation of Italian financial interests.

The stakes are high. MPS, after years of restructuring and state intervention, has emerged as a leaner, more profitable entity with a revitalized distribution network. For Generali, gaining access to the MPS branch network isn't just about insurance; it’s about capturing a larger share of the Italy private banking market 2026 and beyond.

The complexity of this "boardroom chess" is heightened by the influence of heavyweight shareholders. Figures like Francesco Gaetano Caltagirone and the Delfin holding (the Del Vecchio family) have long advocated for a stronger, more "Italian" Generali. Their influence, combined with the strategic positioning of Mediobanca, creates a powerful momentum toward domestic consolidation. The challenge, however, remains the timing. MPS is facing a leadership turnover with a CEO succession scheduled for April, which could influence the speed and direction of any partnership negotiations.

| Feature | Current AXA Partnership | Proposed Generali Partnership |

|---|---|---|

| Origin | French / Multinational | Italian / Domestic |

| Strategic Goal | Cross-border market share | Financial Sovereignty & Consolidation |

| Network Access | Exclusive distribution at MPS | Integrated domestic wealth platform |

| Focus | Standardized insurance products | Bespoke wealth & "Sovereign" asset management |

The €300 Billion Opportunity: Italy’s Great Wealth Transfer

The primary driver behind this strategic maneuvering is a demographic inevitability often referred to as the "Great Wealth Transfer." Italy possesses one of the highest concentrations of private wealth in the world, but that wealth is currently skewed toward an aging demographic.

Currently, approximately 75% of Italy's total private wealth is held by individuals over the age of 55. Over the next decade, this is expected to trigger a massive inter-generational shift. Analysts estimate that by 2033, roughly €300 billion in assets will pass from the "Silent Generation" and Baby Boomers to their Gen X and Millennial heirs.

The Numbers: Italy’s Generational Shift

- €300 Billion: Total assets expected to change hands by 2033.

- 75%: Percentage of private wealth held by those over 55 today.

- 6%: Projected annual growth rate for the private banking sector through 2026.

For Generali, capturing this transfer is essential. Younger heirs tend to have different investment priorities than their parents; they are more likely to seek ESG-aligned portfolios, digital-first advisory services, and sophisticated wealth preservation strategies. If Italian institutions don't step in with a compelling, modern value proposition, this capital risks leaking into global fintech platforms or foreign private banks. Managing Italian household savings management at this juncture is a defensive play as much as an offensive one.

A Structural Growth Engine: Italy's Private Banking Outlook 2026

The Italian private banking sector is no longer a sleepy corner of the financial world. It has become a structural growth engine for the national economy. With total assets under management projected to surpass €1.4 trillion by 2026, the demand for high-quality advisory services is skyrocketing.

This growth is driven by a shift in how Italians view their money. Traditionally, Italian households favored government bonds (BOTs) and real estate. However, with the return of inflation and the complexity of global markets, there is a marked transition toward managed solutions. Italian banks and insurers are reshaping their models to meet the expectations of High-Net-Worth Individuals (HNWIs) who demand more than just a savings account.

The evolution includes:

- Integrated Advisory: Moving beyond simple investment products to offer tax planning, legal support, and succession advice.

- Human + AI: Leveraging artificial intelligence to provide data-driven insights while maintaining the high-touch "human" element that Italian clients value.

- Alternative Assets: Increasing allocation to private equity and private debt to seek returns in a volatile public market.

Recommended: Look for a market sentiment chart showing the steady incline of Italian AuM since 2020. The trajectory clearly illustrates why the Generali vs AXA insurance deal is being fought so fiercely—the "prize" of the Italian balance sheet is growing larger every year.

Beyond Cash: Real Estate and the 'Flat Tax' Factor

When we talk about Italian wealth, we cannot ignore the "trophy assets"—the historic villas, luxury apartments in Milan, and vineyards in Tuscany. Wealth management in Italy is increasingly a real estate play. Italian domestic firms have a natural advantage here, possessing the local network and cultural nuance required to manage these complex assets.

Furthermore, Italy has become a magnet for global HNWI capital due to strategic tax incentives. The "Flat Tax" for new residents—recently updated to €200,000 to €300,000 per year for foreign income—has attracted ultra-wealthy individuals to Rome, Milan, and Tuscany. This influx of global capital requires sophisticated domestic management, further strengthening the case for a dominant Italian wealth champion like Generali. Italy’s ranking in the global wealth map is rising, with its major cities consistently appearing in the top 30 for luxury housing and private wealth concentration.

Conclusion: Sovereignty vs. Globalism in European Finance

The battle for the MPS partnership is a microcosm of a larger debate happening across Europe: the tension between economic globalism and the need for national financial champions. If Generali succeeds in its quest, it will create a powerful precedent for financial sovereignty Italy. It would signal that Italian savings should be the engine that fuels Italian growth, managed by institutions that are deeply rooted in the nation’s social and economic fabric.

While the "economics" of the deal—the price and the profit margins—will always be the headline in financial papers, the "control" aspect is what matters for the long term. As we look toward 2026 and 2027, the outcome of the MPS deal will likely trigger a broader wave of Italian banking consolidation. Whether UniCredit or other players join this dance remains to be seen, but one thing is clear: the era of allowing Italian household savings to be a passive asset managed from abroad is coming to an end.

FAQ

Why is Generali specifically targeting the MPS partnership?

Generali wants to expand its distribution network and increase its market share in the Italian private banking sector. By replacing AXA at MPS, Generali secures a direct line to a massive base of Italian household savings, which is essential for its long-term growth and its goal of domestic financial sovereignty.

What does the 'Great Wealth Transfer' mean for regular investors?

For investors and heirs, this transfer represents a shift toward more modern, diversified, and managed portfolios. It means that traditional ways of holding wealth (like simple cash or property) are being replaced by sophisticated advisory services that focus on tax efficiency and inter-generational planning.

How does the 'Flat Tax' impact the Italian wealth market?

The Flat Tax is a policy designed to attract high-net-worth individuals to move their residency to Italy. By paying a fixed annual sum on foreign income, these individuals bring significant capital into the Italian ecosystem, boosting the demand for luxury real estate and high-end private banking services.