Quick Facts

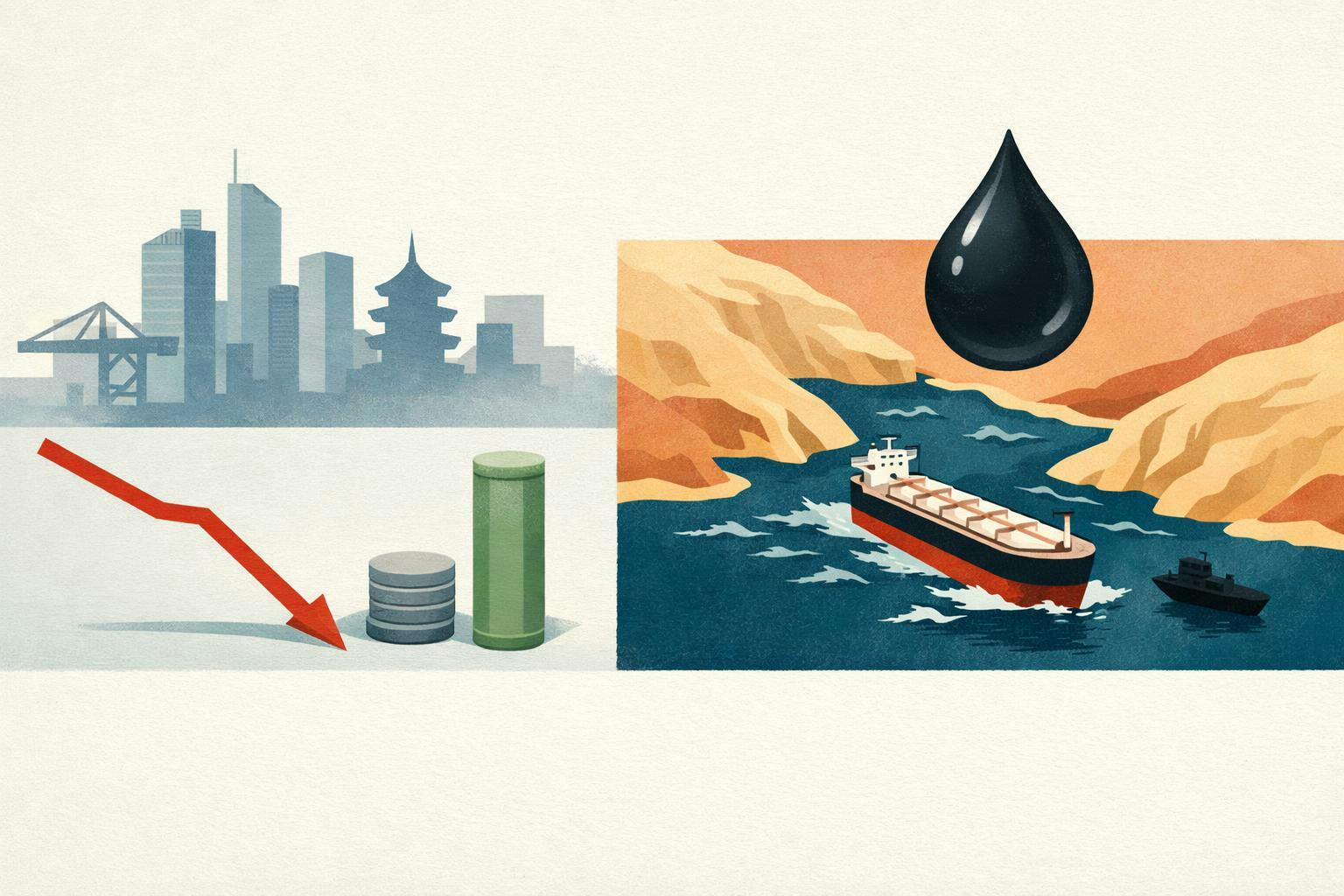

- The Chokepoint: The Strait of Hormuz is the world's most sensitive oil artery, facilitating the transit of approximately 20% of the world's total oil supply.

- The Price Spike: Crude oil prices surged by roughly 9% in a matter of days, breaching the psychological $100-per-barrel threshold following heightened maritime security risks.

- Inflation Link: For every $10 increase in the price of a barrel of crude, consumers typically see an addition of roughly 30 cents per gallon at the pump.

- Investment Shift: Energy shocks often trigger a "flight to quality," strengthening the US dollar while putting significant pressure on energy-importing emerging markets.

- Monetary Policy: Sustained prices above $100 threaten to derail the "disinflation" narrative, likely forcing central banks to postpone anticipated interest rate cuts.

The global energy market has just received a stark reminder of its own fragility. For much of the past year, investors focused on cooling inflation and the potential for a "soft landing." However, as crude oil barrels past the $100 mark, the narrative has shifted from growth optimism to risk management. As an editor specializing in portfolio strategy, I see this not just as a commodity story, but as a systemic shift that redefines the "higher-for-longer" interest rate environment. When energy costs spike, they act as a regressive tax on consumers and a margin squeeze on corporations, effectively tying the hands of central banks globally.

The Trigger: Why Oil Surged Above $100

The primary catalyst for this sudden volatility is the escalating security risk surrounding the Strait of Hormuz. Often referred to as the "world's oil jugular," this narrow waterway is the only sea passage from the Persian Gulf to the open ocean. It handles roughly 20% of global oil flows, making it the single most important chokepoint in the global energy supply chain. When shipping insurance premiums rise or transit is threatened, the market reacts with immediate, defensive pricing.

The recent 9% jump in crude prices isn’t just about supply-and-demand fundamentals; it is about the "risk premium." Investors are pricing in the possibility of a protracted disruption. In historical terms, we are seeing a risk premium similar to the levels observed during the early stages of the 2022 Russia-Ukraine conflict or the 1990 Gulf War. Unlike those events, however, the global economy today is already wrestling with high debt loads and a fragile post-pandemic recovery, making this specific shock particularly difficult to absorb.

Market Reaction and Equity Volatility

The equity markets have responded with a predictable bout of indigestion. While energy stocks have naturally seen an uptick, the broader market is grappling with the implications of higher input costs. For companies that rely heavily on logistics—from e-commerce giants to traditional manufacturers—the prospect of sustained high fuel costs represents a direct hit to the bottom line.

Global Economic Impact: The New Inflation Risk

The most immediate danger of crude oil above $100 is the "Inflation Trap." Energy is a ubiquitous input; it powers the trucks that deliver groceries, the planes that move cargo, and the factories that produce consumer goods. When energy prices rise, those costs are almost invariably passed down the supply chain. This is what economists call "second-round effects."

For central banks like the Federal Reserve and the European Central Bank (ECB), this is a nightmare scenario. They have spent the last two years trying to anchor inflation expectations. A renewed energy shock could cause inflation to become "sticky," discouraging central banks from cutting interest rates even if the economy begins to slow.

- The Federal Reserve: Likely to adopt a "wait and see" stance, potentially delaying rate cuts until the energy-driven inflation spike proves transitory or manageable.

- The ECB: Facing a more difficult path, as the Eurozone is a net energy importer. High energy prices can cause "stagflation"—low growth combined with high inflation.

- US Dollar Strength: Energy shocks typically drive investors toward the safety of the US dollar. While this helps the US manage its own import costs, it creates a "double-whammy" for emerging market energy impacts, as their local currencies weaken just as their fuel bills (denominated in USD) rise.

Regional Winners and Losers: A Comparative Analysis

Not all economies are created equal when it comes to an oil price shock 2026. The impact is heavily dictated by a nation's energy intensity and its status as a net importer or exporter. While the US has become a significant energy producer, regions like Europe and North Asia remain deeply vulnerable to price spikes.

| Region | Vulnerability | Recession Threshold | Strategic Outlook |

|---|---|---|---|

| United States | Moderate | $150 / barrel | High domestic production provides a buffer; consumer resilience remains key. |

| Euro Area | High | $120 / barrel | Dependence on imports makes the region prone to a rapid GDP hit (est. 1% drop). |

| Japan | High | $115 / barrel | Almost entirely dependent on energy imports; likely to see significant trade deficit expansion. |

| Emerging Markets | Very High | Varies | Risk of currency crises as energy costs soar and the USD strengthens. |

The US economy remains remarkably resilient, with an estimated recession threshold as high as $150 per barrel. This is due to the shift in the US's role as a global energy powerhouse. However, for Japan and the Euro Area, the margin for error is much thinner. A sustained price of $125 per barrel could easily shave a full percentage point off Eurozone GDP, pushing several member states into a technical recession.

The Consumer Impact: From Oil Barrels to Gas Pumps

For the average household, the macroeconomics of the Strait of Hormuz translate directly to the price listed on the corner gas station's marquee. The "Gasoline Math" is relatively straightforward but painful: market data suggests that every $10 increase in oil adds roughly 30 cents per gallon at the pump.

However, the impact is not distributed evenly. We are seeing what I call a "K-shaped energy impact":

- Lower-Income Households: Energy and food costs represent a much larger share of the monthly budget. For the bottom 60% of earners, energy-related costs can account for 4% of take-home pay, compared to just 2% for top earners.

- Middle-Class Discretionary Spending: When it costs $20 more to fill up a tank, that is $20 not spent at a restaurant or on a retail purchase. This "crowding out" effect can slow down the consumer-driven service sector.

- Secondary Supply Chain Costs: It’s not just the car; it’s the contents of the grocery cart. Rising diesel prices increase the "last-mile" delivery costs for everything from milk to electronics, ensuring that the global inflation risks are felt at the checkout counter.

Portfolio Tip: During energy-driven inflation cycles, "Value" stocks in the energy and materials sectors often outperform "Growth" stocks, which are more sensitive to the rising interest rates that often follow inflation spikes.

Strategic Outlook: Investment Implications

As a strategy editor, my advice to long-term investors is to avoid knee-jerk reactions, but to acknowledge that the "lower-for-longer" interest rate dream may be on hold. If oil remains above $100, the investment playbook must adapt to a "higher-for-longer" inflation reality.

Identifying the Hedges

Energy and Materials remain the most logical hedges against supply-side shocks. These sectors possess "natural pricing power"—they are the first to benefit from rising commodity prices. Diversified energy producers with strong balance sheets are particularly well-positioned to weather the volatility while providing dividends that can offset losses in other parts of a portfolio.

The Margin Squeeze

Investors should be cautious about sectors with high transport and energy inputs.

- Airlines & Logistics: Fuel is often their largest variable expense.

- Shipping-Heavy Manufacturing: Increased freight costs will eat into margins.

- Consumer Discretionary: As consumers spend more on essentials, "nice-to-have" spending often declines.

Defensive Positioning

In this environment, shifting toward assets that can withstand tighter financial conditions is prudent. Look for high-quality companies with low debt and stable cash flows. In fixed income, shorter-duration bonds may be preferable as the risk of the Fed staying "restrictive" for longer increases the volatility of long-term yields.

FAQ

Q: Why does a conflict in the Strait of Hormuz affect my local gas prices so quickly? A: Oil is a globally traded commodity. Even if your local gas comes from domestic sources, the global price is set by the most expensive "marginal" barrel. When a major artery like the Strait of Hormuz—handling 20% of global flow—is at risk, the global supply-demand balance tightens instantly, driving up prices everywhere.

Q: Will the US release more oil from the Strategic Petroleum Reserve (SPR) to lower prices? A: While the SPR is a tool available to the government, its effectiveness depends on the scale of the disruption. Releasing oil can provide short-term relief, but it does not solve the long-term geopolitical risks or the underlying supply constraints caused by shipping disruptions.

Q: How does a stronger US dollar affect oil prices? A: Oil is priced in US dollars. Historically, there is an inverse relationship: a stronger dollar usually makes oil more expensive for countries using other currencies, which can dampen global demand. However, during an oil price shock, both the dollar and oil prices often rise together as investors seek safety in the USD while reacting to the supply shortage in oil.

Action Plan for Investors

- Rebalance Energy Exposure: Ensure your portfolio has sufficient exposure to the energy sector to act as a hedge against rising consumer costs.

- Review Interest Rate Sensitivity: Evaluate your holdings in tech and growth-oriented sectors that may suffer if central banks delay interest rate cuts.

- Monitor Currency Risks: If you hold international stocks, be aware that a rising US dollar could negatively impact the returns of companies based in energy-importing emerging markets.

- Stay Informed on Geopolitics: In a "macro-driven" market, events in the Strait of Hormuz are just as important as corporate earnings reports. Keep a close eye on shipping data and regional security updates.

The current oil price shock is a reminder that the path to economic stability is rarely a straight line. By understanding the links between geopolitical chokepoints, inflation, and monetary policy, investors can better position their portfolios to navigate the volatility of a $100+ crude oil world.