Quick Facts

- The 5% Rule: Most private credit funds, including popular Business Development Companies (BDCs), limit quarterly redemptions to 5% of their total Net Asset Value (NAV).

- The $2 Trillion Shift: Private credit has surged into a $2 trillion industry, moving systemic financial risk from traditional banks directly onto the balance sheets of yield-seeking retail investors.

- Gating Mechanics: If total withdrawal requests exceed the 5% cap, investors receive a "pro-rata" share, meaning you might only get 20% or 30% of the cash you asked for in a given quarter.

- Duration Mismatch: These funds invest in loans with 3-to-5-year terms but offer quarterly liquidity—a structural tension that market analysts expect will lead to redemption backlogs lasting 3 to 5 quarters through 2026.

Introduction: The $2 Trillion Stress Test

For years, private credit was the exclusive playground of institutional titans—pension funds and endowments with decades-long horizons. But the landscape has shifted. Today, the "democratization" of private equity has funneled billions of dollars from individual brokerage accounts into private debt. This has transformed a once-niche corner of the market into a $2 trillion powerhouse.

However, as we move through 2026, this rapid growth is meeting its first significant hurdle: the liquidity stress test. Investors who were lured by steady 10% yields are now discovering the fine print. The "liquidity promise" of semi-liquid funds is being tested by a cooling economy and rising default rates.

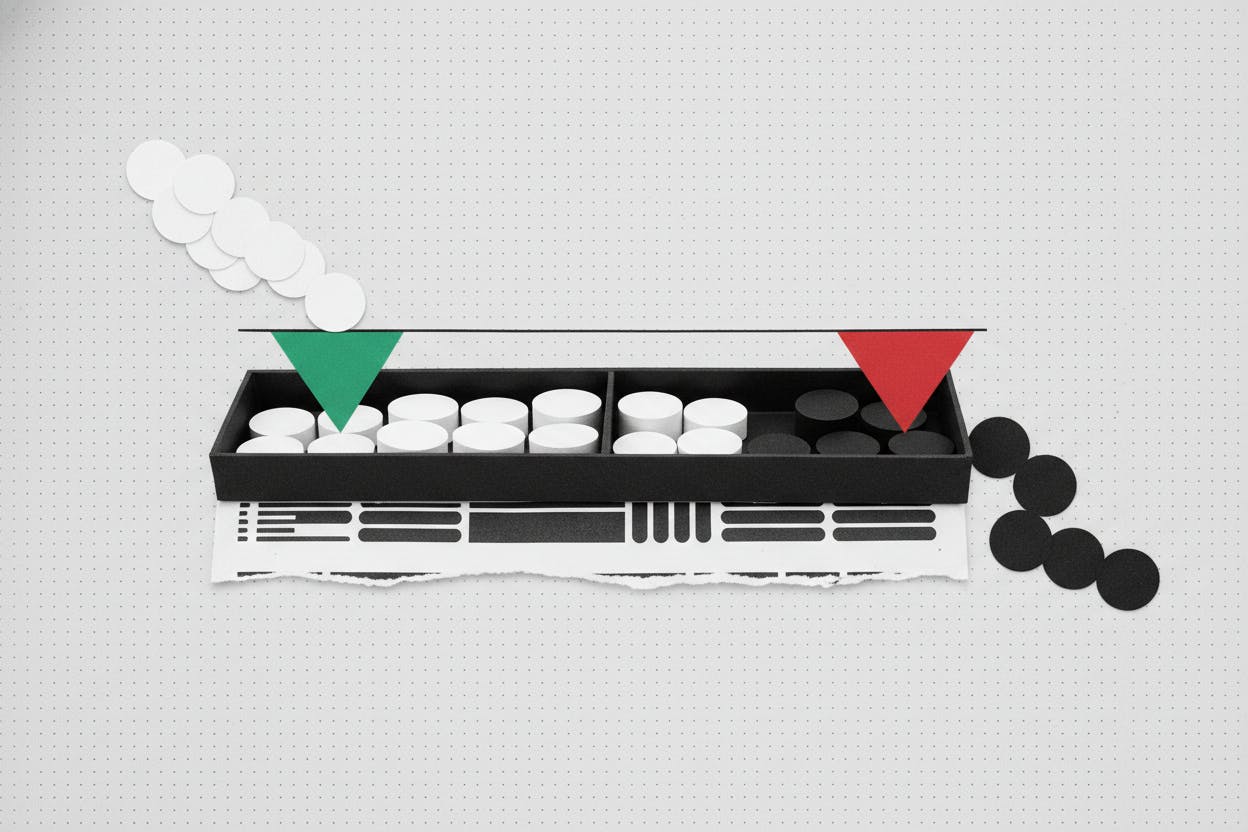

What no one tells you until the "gate" drops is that private credit withdrawal limits are not a sign of fund failure, but a structural necessity. These mechanisms, often called "gates," typically restrict quarterly redemptions to 5% of a fund's NAV. This is designed to prevent a "fire sale" of illiquid loans, but for the individual investor needing immediate cash, it can feel like being trapped in a burning building where the exit door only opens six inches at a time.

Executive Summary: The Reality of Redemption Private credit offers an "illiquidity premium"—extra yield in exchange for locking up your money. When markets get volatile, fund managers use "gates" to protect the remaining shareholders from the costs of forced asset sales. If you invest here, you must view your capital as committed for years, not months.

The Mechanics of the 'Gate': Protecting the Fund or Trapping the Investor?

To understand why your money might be stuck, you have to understand the underlying assets. A private credit fund lends money to mid-sized companies. These loans aren't traded on a public exchange like Apple stock; they are private contracts with terms often lasting three to five years.

There is a fundamental mismatch between a 3-year loan and a quarterly withdrawal request. If a fund allowed everyone to leave at once, it would have to sell those loans to third parties at a massive discount (a fire sale). To prevent this, managers implement withdrawal limits.

This creates two types of redemptions:

- Performance-Driven Redemptions: Investors leave because the fund is underperforming or defaults are rising.

- Market-Driven Redemptions: Investors leave because they need cash for other things (like paying taxes or covering losses in their stock portfolio), regardless of how well the private credit fund is doing.

The "gate" doesn't care why you're leaving. Once the 5% quarterly limit is hit, the gate closes. If the fund receives requests for 10% of its NAV, every investor who asked for money only gets half of what they requested. This "pro-rata" distribution is the reality of the private credit market in 2026.

High-Stakes Reactions: How the Giants are Responding in 2026

The largest players in the industry are currently navigating these waters with different strategies. As default rates tick upward, the pressure to maintain NAV valuations while satisfying panicky investors has led to some high-stakes maneuvers.

| Firm & Fund | Current Strategy | Stance on Liquidity |

|---|---|---|

| BlackRock (HLEND) | Strict 5% NAV Cap | Prioritizing its 10.7% annualized return by refusing to sell assets early. |

| Blackstone (BCRED) | Personal Capital Injections | Using corporate balance sheet strength (up to $400M) to bridge liquidity gaps. |

| Blue Owl | Asset Sales & Gating | Sold $1.4B in assets to meet backlogs; has temporarily suspended withdrawals in select feeder funds. |

BlackRock’s HLEND, for instance, has remained firm on its 5% cap. From a portfolio strategy perspective, this is the "correct" move—it protects the 10.7% yield for those who stay. However, for the investor who needs that 10% of their principal today, the policy feels restrictive.

Blackstone has taken a more aggressive approach to maintaining investor confidence, occasionally using its own capital to ensure redemptions are met or to signal strength. But even giants have limits. When the volume of requests stays high for multiple quarters, even a $400 million cushion can start to look thin.

Looking Beyond the Gates: What History Tells Us

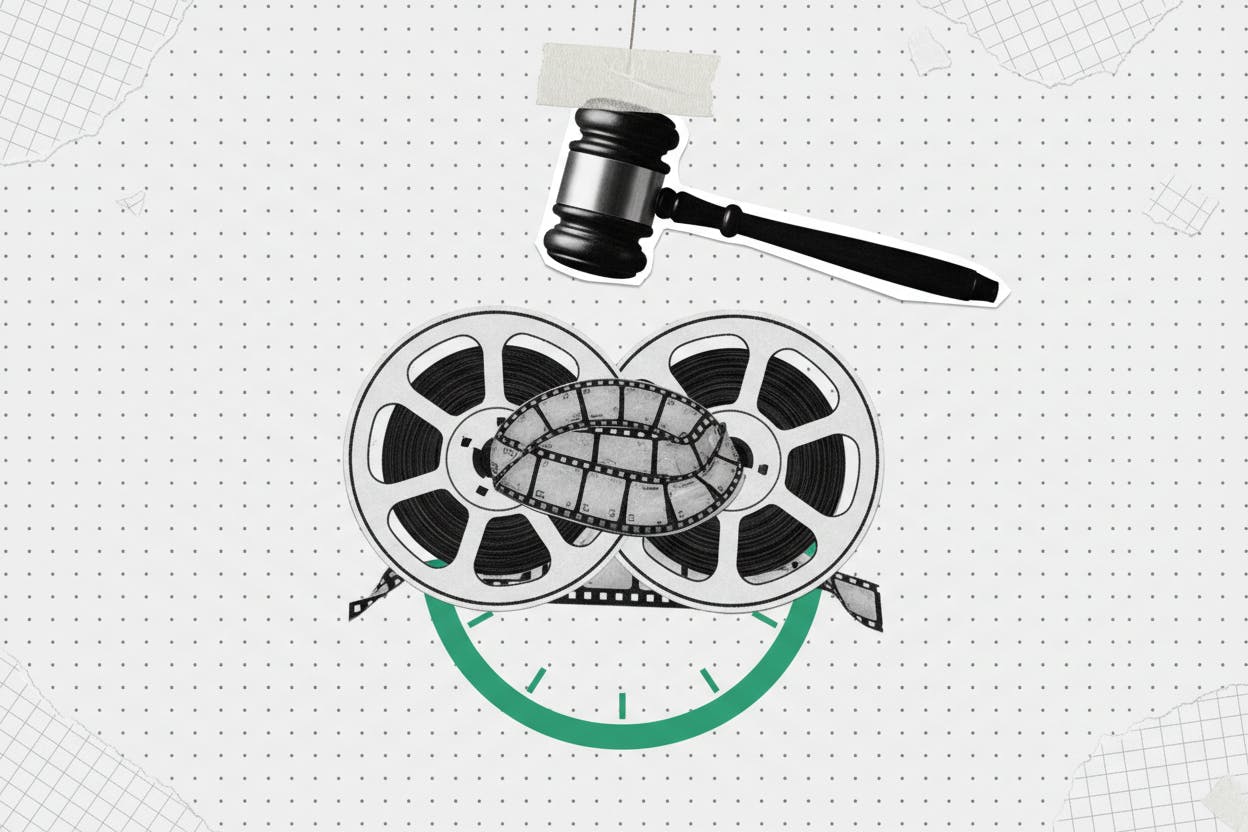

We don't have to guess how this ends; we can look at the "BREIT" case study. Blackstone’s Real Estate Income Trust (BREIT) faced a similar liquidity crunch starting in late 2022. As investors rushed for the exits, the fund began rationing withdrawals.

It took 14 months for BREIT to fulfill 100% of the redemption requests it received during that peak period. This is the "What No One Tells You" part: even if the assets are high quality, the process of getting your money back can take over a year.

During a pro-rata cycle, your experience looks like this:

- Quarter 1: You ask for $100,000. The fund is 2x oversubscribed. You receive $50,000.

- Quarter 2: You submit for the remaining $50,000. Requests are still high. You receive $20,000.

- Quarter 3: You finally receive the remaining $30,000.

In the meantime, the NAV of the fund might fluctuate. You aren't just waiting for your cash; you are waiting while being exposed to the risk of the fund's value dropping before you can exit completely.

Stats at a Glance

- Market Growth: $2 Trillion (Up from $1.2T in 2020)

- Typical Gate: 5% of NAV per quarter

- Default Rate Trend: Rising toward 4.5% for mid-market borrowers

- Liquidity Wait Time: 3-5 quarters (estimated for 2026 oversubscriptions)

Scenario Analysis: The 2026-2027 Outlook

As we look toward the remainder of 2026 and into 2027, several factors are converging to make private credit withdrawal limits a recurring headline.

First, the "repricing" of risk is in full swing. Many of the loans made in 2021 and 2022 at low interest rates are now struggling to service their debt at today's higher rates. Industry analysts estimate that if redemption requests remain at current levels, oversubscriptions in major BDCs could persist for 3 to 5 quarters.

Second, the impact of rising default rates on fund valuations cannot be ignored. When a fund "marks down" the value of its loans, its NAV drops. If you are waiting in a redemption queue, a falling NAV means you are getting back a fraction of a smaller pie. Furthermore, as funds gate redemptions, their fee income—often tied to the size of the assets under management—stays inflated, creating a potential conflict of interest between the manager (who wants to keep the assets) and the investor (who wants to leave).

Metrics for the Cautious Investor

If you are currently allocated to private credit or considering an entry, you must look past the "Headline Yield." Strategic investors use two primary lenses:

1. Portfolio-Based Liquidity

Look at the interest yield vs. loan turnover. A healthy fund should have an average interest yield of around 10% and a loan turnover of about 1/3rd of the portfolio annually. If turnover slows down significantly, it means the underlying companies can't refinance their debt, which is a leading indicator that the "gate" is about to close.

2. Structural Liquidity

Examine the debt-to-equity ratio of the fund itself. The average for top-tier BDCs is approximately 0.91x. If a fund is heavily leveraged (closer to 1.25x or higher), it has less "dry powder" to pay out departing investors without being forced to sell assets or borrow more money at expensive rates.

Olivia’s Strategy Tip: Don't treat private credit as your "emergency fund." It belongs in the "illiquid core" of your portfolio. If you might need the cash within 12 months, you are better off in a money market fund or short-term Treasuries, even if you have to sacrifice 4% in yield.

FAQ: Navigating the Liquidity Crunch

Q: Can a fund permanently stop me from withdrawing my money? A: Legally, most BDCs and interval funds have the right to suspend redemptions entirely under extreme market conditions. However, this is a "nuclear option" that severely damages a firm's reputation. Most choose to use the 5% quarterly gate instead.

Q: If I’m in a pro-rata situation, do I have to re-apply for my withdrawal every quarter? A: This depends on the fund's specific bylaws. Some funds "roll over" your request to the next quarter automatically, while others require you to submit a new request. Check your prospectus immediately if you are planning an exit.

Q: Is the 5% limit based on my personal investment or the whole fund? A: It is based on the fund's total Net Asset Value (NAV). If the fund has $10 billion in assets, it will pay out a maximum of $500 million in redemptions that quarter. If investors ask for $1 billion total, everyone gets exactly 50% of what they asked for.

Conclusion

The "feature, or the bug, of these things is you can’t get out right away." This phrase, popularized during the recent real estate liquidity crunch, is the defining reality of private credit in 2026.

Private credit remains a vital tool for portfolio diversification and income generation. However, the days of viewing these funds as "liquid-adjacent" are over. As an investor, your strategy must account for the 5% gate. Treat your private credit allocation like a partnership: easy to enter, but requiring a long, coordinated walk to the exit.

By understanding the mechanics of redemptions and monitoring the structural health of your funds, you can avoid being caught off guard when the gates inevitably move.